Notes on oral arguments 7

District Court of The Hague

| Case number | C/09/571932 2019/379 |

| Session | 15 December 2020 |

Merits of the claim – part 2

in the matter of:

- Vereniging Milieudefensie both on its own behalf, and in its capacity of representative ad litem and representative of the co-complainants who are listed on Annex A, which annex is attached to the summons and forms part thereof, having its registered office in Amsterdam, the Netherlands;

- Stichting Greenpeace Nederland, having its registered office in Amsterdam, the Netherlands;

- Landelijke Vereniging tot Behoud van de Waddenzee, having its registered office in Harlingen, the Netherlands;

- Stichting ter bevordering van de Fossielvrij-beweging, having its registered office in Amsterdam, the Netherlands;

- Stichting Both ENDS, having its registered office in Amsterdam, the Netherlands;

- Jongeren Milieu Actief, having its registered office in Amsterdam, the Netherlands;

- Stichting ActionAid, having its registered office in Amsterdam, the Netherlands.

Claimants

Hereinafter also called: “Milieudefensie et al.”

Counsel:

- Mr R.H.J. Cox

- Mr. D.M.J. Dexters

- Mr. A.J.M. van Diem

- Mr. S.J. Keuls

Versus

Royal Dutch Shell plc

Having its registered office in The Hague, the Netherlands

Defendant

Counsel:

- Mr. D. Horeman

- Mr. J. de Bie Leuveling Tjeenk,

- Mr. N.H. van den Biggelaar

Your Honours,

- The nature of RDS' conduct (criterion 4 of the Kelderluik criteria)

1.a The degree of attribution of scope 1, 2 and 3 emissions

-

Milieudefensie et al. argued in the summons that RDS has control over the scope of the emissions of the Shell group and that RDS also has control over the scope of the emissions that is connected with the energy products that it produces and trades.1 Because of this control and because of the fact that RDS is an important party in the energy transition, Milieudefensie et al. set out arguments in the summons and concluded that the nature of RDS' conduct is comparable to that of the State of the Netherlands in the Urgenda case and that this must lead to a societal duty of care on the part of RDS.2 I will present further substantiation for this component and in particular go into the responsibility that RDS has with regard to the scope 3 emissions over which it has control, just as it does over the scope 1 and 2 emissions. I will first briefly reflect on arguments that have already been presented.

-

The opening arguments discussed the control which RDS has as head of the Shell group in detail. RDS is in charge of the central management of the Shell group, has a direct or indirect controlling interest in the companies belonging to the Shell group and sets out the general policy for the group, including the climate and transition policy. RDS has control over the group investments, weighs its investment choices against the risks of the energy transition and determines the energy portfolio of the Shell group. The control which RDS has in relation to the scope of the emissions and the energy portfolio of the Shell group also follows from RDS' Net Carbon Footprint ambition, which ambition relates to the entire Shell group.3

-

Because of the control over both the scope of the emissions of the Shell group and over the shape of the energy portfolio of the Shell group, RDS has control over both the scope 1 and 2 emissions, and the scope 3 emissions. The scope 1 emissions are the CO2 emissions of the Shell group's own operations. The scope 2 emissions concern, inter alia, the CO2 emissions of the electricity and heat procured by the Shell group. The scope 3 emissions relate, inter alia, to the CO2 emissions of the fossil fuels which the Shell group produces and sells under the management of RDS so that these can be burned by consumers and organisations.4

-

RDS reports annually in various publications on the total scope 1, 2 and 3 emissions of the Shell group and does so on the basis of the guidelines of the Greenhouse Gas Protocol.5 The total of these emissions connected with the Shell group is approx. 1.2% of the global emissions. The scope 1 and 2 emissions form approx. 15% of the total emissions of the Shell group (approx. 0.2% of global emissions) and the scope 3 emissions form approx. 85% of the total emissions of the Shell group (approx. 1% of global emissions). The collective scope 1 and 2 emissions thus matter at global level and the scope 3 emissions do that all the more.

-

In view of both the control which RDS has over the scope 1 and 2 emissions and over the scope 3 emissions of the Shell group, in view of the considerable scope of these emissions and in view of the seriousness of the danger that these emissions create for the claimants and their interests, Milieudefensie et al. believes that RDS is subject to a legal responsibility. A legal responsibility to (partly in view of all other circumstances presented by Milieudefensie et al.) behave in a socially careful manner by bringing this scope of emissions back into conformity with the global emissions reduction scenario that is necessary to be able to achieve the temperature goal of the Paris Agreement.

-

It was pointed out in the summons with regard to the scope 3 emissions that Shell itself acknowledges the responsibility for the emissions of its customers in the 1990s. Shell already understood in the 1990s that it would also have to reduce the emissions of its customers by offering sustainable energy-carrying products to its customers.6 That Shell and other oil and gas companies have the possibility of reducing the scope 3 emissions of the energy products sold by them, appears from the fact that six oil and gas companies have in the meantime included the reduction of their scope 3 emissions in their objectives. In addition to Shell this concerns BP, Repsol, Total, Eni and Equinor.7

-

It is also the most basic logic that the six oil and gas companies have such control over scope 3 emissions, because every company determines independently and of its own volition how many fossil fuels it wishes to sell. If a company sells more fossil fuels, the scope 3 emissions of the company increase. If a company sells fewer fossil fuels, the scope 3 emissions of the company decrease. That RDS has full and total control over the scope 3 emissions of the energy products which it sells, can thus not be a matter of discussion.

-

In the statement of 6 November 2020, with regard to RDS' responsibility for the scope 1 and 2 emissions as well as for the scope 3 emissions of the Shell group, Milieudefensie et al. referred to the analysis which the UN Special Rapporteur on Human Rights and the Environment presented regarding the responsibilities which companies have in relation to the climate approach on the basis of UN Guiding Principles on Business and Human Rights.8 He says in this respect (quote):

71 [..] corporations should comply with the Guiding Principles on Business and Human Rights as they pertain to human rights and climate change. 72. The five main responsibilities of businesses specifically related to climate change are [...]

-

The first responsibility mentioned by the UN Rapporteur concerns the reduction of the scope 1 and 2 emissions. According to the UN Special Rapporteur, companies have the responsibility (quote):

to reduce greenhouse gas emissions from their own activities and their subsidiaries.9

In other words, companies must not only ensure that their own emissions are reduced, but that in addition the emissions of their subsidiaries are reduced. In a general sense, group heads are thus deemed able to reduce the scope 1 and 2 emissions of the group. That is why they have a responsibility to do so, according to the UN Special Rapporteur.

-

The second responsibility which is mentioned is, according to the UN Special Rapporteur, the scope 3 emissions. According to him, companies have the responsibility (quote):

to

reduce greenhouse gas emissions from their products and services.

.10

The UN Special Rapporteur also says that companies thus have control over the products and services that they offer and consequently also have the option and responsibility to reduce the CO2 emissions which are released in the consumption of those products and services.

-

Furthermore, according to the UN Special Rapporteur companies have the responsibility, inter alia, (quote):

to

minimize greenhouse gas emissions from their suppliers.11

The responsibility of companies to ensure that the emissions of their suppliers are reduced, is related to the fact that via their purchasing processes they can set requirements for suppliers. That is why this degree of control, too, leads to a responsibility for companies to reduce emissions, according to the UN Special Rapporteur.

-

The responsibility which the UN Special Rapporteur attributes to companies to reduce the emissions connected with their business activities and products and services because they have the option and responsibility to do so, is also widely supported and acknowledged as necessary climate action of non-state parties which falls under the UN climate regime.

-

The important role of non-state parties under the UN Climate Regime has already been discussed in detail in the opening arguments.12 In this respect it has been pointed out, inter alia, that in 2012 the countries in Work Group 2 came to the conclusion that the emissions gap had to be closed as quickly as possible and that this requires proactive climate action on the part of non-state parties. Under the auspices of the UN, the Non-State Actor Zone for Climate Action was therefore set up in 2014, with the goal of, in addition to state climate action, working on a second action agenda for non-state parties such as investors, companies and cities.

-

As a result of both action agendas, the Climate Ambition Alliance was established in 2019 during the 25th UN Climate Change Conference. In this Climate Ambition Alliance, both state and non-state parties committed themselves to the target of achieving net-zero CO2 emissions in 2050, which is necessary to achieve the Climate Goal of the Paris Agreement. Milieudefensie et al. has submitted the press release on this alliance of state and non-state parties into the proceedings as Exhibit 285. More information on this alliance can be found on the aforementioned Non-State Actor Zone for Climate Action. It is also emphasised there that states cannot handle the task on their own and that non-state action is necessary to achieve the goal of the Paris Agreement and that this should take place taking account of the latest scientific findings (quote):

The overall goal of this group is to push for net-zero CO2 emissions in line with latest scientific information. The deep transformation towards net-zero CO2 emissions requires the mobilization of actors across all segments of society, which is why this group includes regions, cities, businesses, and investors alongside countries. All are united behind the same target because they recognize the benefits of the low-carbon transition.13

-

In order to achieve the necessary expansion of the group of non-state parties within the Climate Ambition Alliance as quickly as possible, the "Race to Zero" initiative was developed under the auspices of the UN. In this Race to Zero initiative the global networks were brought together which have developed emissions reduction protocols and guidelines for non-state parties. On the basis of scientific findings these protocols and guidelines show, inter alia, what companies have to do to take responsibility for reducing the emissions which are attached to their activities and products.14 Companies can only participate in this UN-facilitated initiative via application of these protocols and guidelines.

-

Oxford University made an analysis in connection with this Race to Zero initiative of the various protocols and guidelines for non-state actors. The Oxford analysis indicates the points on which there is consensus between the various protocols and guidelines and the points regarding which some questions still remain. The consensus charted by the Oxford analysis shows that the elaboration of the UN Guiding Principles by the UN Special Rapporteur is widely supported. Milieudefensie et al. has submitted the Oxford analysis and the Race to Zero paper into the proceedings as Exhibit 287. The following appears from this.

-

First, according to the Oxford analysis there is consensus in a general sense that emissions reduction targets of companies according to the guidelines and protocols must encompass all business activities and all scopes, i.e. scope 1, 2 and 3.15 This underlines the accuracy of the approach chosen by the UN Special Rapporteur that it is necessary under the UN Guiding Principles that multinational companies not only lower their group emissions, but that they must also reduce the scope 3 emissions of the products and services which they offer on the global market.

-

Second, the Oxford analysis shows that there is consensus that the target to be achieved, is the target of net-zero CO2 emissions in 2050. It is emphasised in this respect that there can be no delay and that therefore an immediate start must be made with reducing CO2 emissions. Companies thus cannot keep kicking the can down the road when it comes to the task to reduce emissions. In addition, the importance of concrete robust interim reduction targets for the short- and mid-term is emphasised.16 The Oxford study also sets out that it is not only important to achieve the net-zero target, but that the reduction path to be followed to the net-zero point is relevant (quote):

A net-zero target implies not just an outcome in 2050 but a commitment to a multi-decade pathway of emissions reductions. > Interim targets are important complements to long-term net zero targets. >Immediate action is needed on all net-zero targets..17

-

I will speak about the importance of the reduction path to the net-zero point later. The path to the net-zero point and the interim reduction targets to be achieved is fully decisive for the quantity of emissions which will be cumulatively added to the atmosphere in the coming decades. In short, the issue is that the faster and more in-depth the reduction in the first phase, the fewer the emissions that will be emitted over the entire period up to the net-zero point. I will make this clear on the basis of a figure later.

-

Third, the Oxford study states that there is consensus that every party will independently have to work toward net-zero emissions, but that per company the scope and timing can vary depending on the capacity and responsibility of the company in question. The explanatory note has the following to say about this (quote):

There is broad agreement that all actors should pursue net zero, but also that various factors may lead various actors to adopt targets differentiated by timing and scope. One, there is wide consensus that capacity should be a key factor in determining the scope and timing of commitments, with those with higher capacity (e.g. developed jurisdictions, larger companies) taking more aggressive and expansive targets. Two, several respondents submitted that historical responsibility and past behavior should also be a relevant consideration [...] Three, respondents also noted that larger emitters should be required to meet more stringent standards than smaller entities..18 (underlining added by counsel)

-

The Oxford analysis thus shows that the guidelines and protocols of the various instances place the greatest responsibility with the biggest CO2 emitters. This particularly applies with regard to the big CO2-emitting companies in the developed jurisdictions because they have the greatest capacity to reduce emissions and have the greatest capacity to bear the financial burdens thereof. These companies must therefore reduce most aggressively of all companies. According to some guidelines, the historic responsibility for CO2 emissions and past conduct are factors which must be taken into account.

-

RDS in particular belongs in the group of biggest CO2 polluters in the world, is one of the richest companies in the world, is based in a developed jurisdiction and has caused substantial historic CO2 pollution. When it comes to conduct of the past, a substantial reproach can be made against its actions, certainly since 2007, as Milieudefensie et al. discussed in the summons and summarised in the statement of 6 November 2020. Precisely for RDS it is reasonable, bearing in mind the conclusions of the UN Rapporteur on the responsibilities of companies under the UN Guiding Principles, to seek an order to reduce emissions which covers the scope 1, the scope 2 and the scope 3 emissions of the entire group over which RDS has the management and control. This is all the more reasonable because the scope 3 emissions of the Shell group constitute 85% of the total emissions. According to the guidelines and protocols, it is precisely in those cases in which the scope 3 emissions form the bulk, that the reduction of scope 3 emissions is appropriate. The Race to Zero paper has the following to say about this (quote):

Net zero pledges to be included under the Race to Zero campaign should: - Cover all emissions, including Scope 3 emissions for businesses and investors where they are material to total emissions [...]19

-

In this respect I will later discuss that RDS itself also believes that it belongs to the part of the global society which must take quicker action because the company, according to its own statements, can do so and has the capacity to do so. What is more, for years RDS has been stating in its annual reports that it is resilient enough to take on the Paris climate goals, thus this too shows that the company has the capacity and options to implement the court order to reduce emissions that Milieudefensie et al. is seeking. I will come back to this.

-

That RDS is responsible for the scope 1 and 2 emissions and also for the scope 3 emissions of the Shell group is thus not only argued by Milieudefensie et al., but also follows from an accurate and reasonable elaboration of the UN Guiding Principles for Business and Human Rights as described by the UN Special Rapporteur on Human Rights and the Environment in his report of 2019.20

-

In the Oxford analysis it is furthermore pointed out that the reduction targets can only be successfully achieved if the obligations are taken on by the CEO and/or the executive board of the company and the CEO and the board provide concrete and specific plans with operational implications. There is furthermore wide consensus that public account must be presented regarding the progress and the achieving of the goals in the short- and mid-term, and there is also consensus that this public accountability should also best take place via the UN Climate Action platform for non-state actors.21 In this manner the second action agenda of the non-state parties is made visible to everyone via the UN platform. This is deemed to be of great importance.

-

As has already been explained in the opening arguments, the idea behind making climate action of non-state actors visible is to create a flywheel effect so that climate action of the other non-state actors but also climate action of the state actors is easier to increase and accelerate.22 Lead by example is the motto. This also shows that the international community expects that if the bigger companies were to voluntarily take on far-reaching climate action or (as via this case against RDS) were obliged to do so, this will result in a flywheel effect. The effect thereof expected by the international community is that other non-state parties, but also state actors, will be more inclined to take farther-reaching action. Attention was paid to this in the opening arguments with regard to the discussion of the important role of non-state actors in solving the climate problem.23

-

In this respect I will briefly come back to a previous remark that not only can it be established that RDS has control over the scope 1, 2 and 3 emissions of its energy products, but it can also be determined that the control which RDS has over its scope 1, 2 and 3 emissions is greater and more direct than the control which the State of the Netherlands has over the emissions of its citizens and companies.24 Because of that more direct and greater control, companies can take more ambitious and quicker action than many national states, according to Chatham House, the Royal Institute of International Affairs.25 This thus enables companies like RDS to create a flywheel effect as soon as they take their responsibility or are obliged to do so. If an order is made against RDS, the effect thereof on other parties will have a global reach because of the worldwide presence of the Shell group and the worldwide sale of its energy products.

-

According to John Ruggie, the man behind the UN Guiding Principles on Business and Human Rights, multinational companies have the exceptional possibility of quick and direct influencing of many parties, including their group companies, their suppliers, their contracting parties and all other stakeholders in the group. This gives them a form of influence which states and intergovernmental organisations do not have. I quote John Ruggie (quote):

[M]ultinationals have authority that states lack. For example, through their codes of conduct they can require suppliers in host states to adhere to social and environmental standards that, if imposed by the country importing those products, the host state could challenge as a non-tariff barrier under the WTO. The ability of multinationals to enforce such "internal" decisions across countries is the envy of states and intergovernmental organizations. The authority of multinationals is not limited to their subsidiaries and affiliates. It also extends to contractors, franchisees, and other types of non-equity counterparties.26 (underlining added by counsel)

-

RDS' influence thus reaches farther than RDS' influence on the Shell group and on the Shell products. RDS has this farther-reaching influence because of its enormous size and the related power position and purchasing position on the global market, including in relation to its suppliers, its contracting parties and other relations of the Shell group. As one of the biggest market parties in the world, RDS has a significant influence in all company chains of which it forms part. It has an influence on what the consumer of the globally operating Shell group is offered in the form of energy products and it has an influence on the suppliers which supply to the Shell group. In this respect I would like to clarify the following in relation to the scope 3 emissions.

-

Milieudefensie et al. has submitted a report of best practices on Scope 3 management as Exhibit 322.27 It is a report that was published by the Science Based Targets Initiative which, as one of the leading networks, is supported by the UN Climate Change Secretariat and by the United Nations Development Programme (UNDP).28 It is a joint venture between, inter alia, the CDP (the Carbon Disclosure Project to which RDS too submits reports every year), the United Nations Global Compact, the World Wildlife Fund and the World Resources Institute.29 I will hereinafter refer to the report of the Science Based Targets Initiative as the SBTI report.

-

The SBTI report states, quote:

Companies must help to prevent the worst impacts of climate change by reducing their greenhouse gas (GHG) emissions as much and as quickly as possible, including reducing value chain (i.e. scope 3) emissions. Scope 3 emissions often represent the largest portion of companies' GHG inventories.30

-

The SBTI report states the following about the need to reduce the scope 3 emissions because of the Paris goal, quote:

In order to mitigate the worst effects of climate change, the global community must take swift and systemic action to reduce its emissions [...] The business community is responsible for the majority of global emissions and must do its part to meet this goal. There is a growing urgency to reduce GHG emissions wherever possible and this includes reducing scope 3 emissions in addition to scope 1 and 2 emissions. [...] There is enormous potential to reduce scope 3 emissions, which would help preserve the rapidly shrinking global carbon budget.31

-

Bearing this rapidly shrinking global carbon budget in mind, the SBTI report then clarifies that the best practice is for companies to reduce the absolute scope of scope 3 emissions. Not only must the reductions be reduced in an absolute sense according to the report, but at a minimum the same targets must also be applied in this respect as those which are globally necessary to achieve the Paris goal. I quote the SBTI report:

Best practices in defining scope 3 target ambition would entail setting targets that are, at a minimum, in line with the percentage reduction of absolute GHG emissions required at a global level over the target timeframe.32

-

Thus if the global emissions must have been reduced in an absolute sense in 2030 by 45%, it is the best practise for companies to also reduce their scope 3 emissions in an absolute sense by 45% by 2030. Only in this manner will it be possible to remain within the limited remaining carbon budget. The absolute emissions reductions to be applied by the companies will be set off against a base year as starting point, so that the absolute emissions reduction can be calculated over a specific period.33 I will come back to the necessity of a base year in the discussion of the claims.

-

The scope 3 emissions of the Shell group encompass approx. 85% of the total emissions of the Shell group.34 On its website RDS allows inspection of the exact numbers of the scope 3 emissions of the Shell group.35 This shows that more than 90% of the scope 3 emissions of the Shell group consist of the emissions which are connected with the use of fossil fuels sold by Shell. In the jargon those emissions, due to use of sold products, are referred to as Scope 3, category 11 emissions.36 These scope 3, category 11 emissions are thus over 90% of the scope 3 emissions. The other 10% of the scope 3 emissions concern the other 14 categories which belong to the scope 3 emissions. This concerns, for example, the emissions of assets which the Shell group leases from other parties, the emissions connected with business travel of Shell staff and the emissions of goods and services procured by the Shell group.37

-

RDS' control over the scope 3, category 11 emissions, i.e. RDS' control over the emissions of the products which the Shell group sells, has already been discussed in detail. This control thus covers over 90% of all scope 3 emissions. According to the SBTI report, RDS has a sufficient degree of control over the other 14 categories which fall under scope 3 emissions, and which together form almost 10% in scope 3 emissions. The SBTI report's conclusion is in the same vein, in line with the above-cited statement of John Ruggie, i.e. that thanks to their strong position in the market, multinational companies can set requirements via their terms and conditions and codes of conduct for suppliers and other chain partners. The report explains that because of their powerful position, the biggest multinational companies can, if necessary, impose their terms and conditions on third parties and enforce them.38

-

RDS makes use of that position, as has been set out, inter alia, in the summons under para. 693, where it was made clear that RDS has not only committed itself to the UN Guiding Principles on Business and Human Rights, but also imposed the compliance therewith on its entire personnel and on all its contracting parties.

-

For RDS the dictating of the conduct of its contracting parties is also crucial because the conduct desired by RDS of its contracting parties is connected with one of the three strategic pillars of RDS, i.e. retaining societal legitimacy for its business activities. This has already been explained in the opening arguments.39 Last year Mr Van Beurden worded this relationship between the conduct of Shell's contracting parties and the retention of societal legitimacy for Shell as follows:

Without a strong societal licence to operate, without trust, we cannot and will not be a world-class investment case nor thrive through the energy transition. Securing a strong societal licence to operate requires three things: The first is to cause no harm to people and no harm to the environment. These are the basics of being in business. It requires strong operational HSSE performance. It requires ethical and respectful behaviours by all our staff and contractors.40

-

Should the District Court decide to order RDS to reduce its emissions, as is being requested by Milieudefensie et al., RDS can and will, by means of its contracting positions and the general position of power which it has as one of the biggest companies in the world, also demand modified actions on the part of its employees and its global contracting parties. In the manners discussed here RDS thus also has a sufficient degree of control over the small 10% in scope 3 emissions which are not connected to the Shell products it sells.

-

By means of all of the foregoing Milieudefensie et al., in its opinion, in addition to what has already been asserted in the summons, the statement of 6 November 2020, the opening arguments and the first hour of this morning of day 3 of the multi-day oral arguments, has substantiated to a sufficient degree that RDS has control over the scope 1, 2 and 3 emissions of the Shell group and therefore has responsibility for these emissions.

1.b The CO2 emissions of the Shell group continue to increase

-

While it is evidently necessary that RDS must drastically reduce the scope of emissions of the operating activities and the products of the Shell group in absolute terms to be able to stay within the rapidly shrinking global carbon budget, and that this is also best practice, RDS has no intention whatsoever to reduce the scope of emissions of the Shell group in the coming decade. On the contrary, up to at least 2030 RDS intends to implement a growth strategy for its oil and gas activities whereby the CO2 emissions of the Shell group will continue to increase. The Net Carbon Footprint ambition which RDS has set for itself, even if it were followed and achieved, will therefore not see the scope of the CO2 emissions of the Shell group be reduced. Milieudefensie et al. made it clear in the summons that only absolute emissions reductions count and are relevant in preventing dangerous climate change and I will now further clarify this against the background of the RDS concern strategy.

-

As Milieudefensie et al. asserted in the statement of 6 November, RDS has a growth strategy whereby the oil and gas production will continue increasing up to 2030 by 38%. This same growth percentage of 38% is mentioned in the shareholders' resolution of Follow This, which was discussed by RDS in May 2020.41 Nor is this growth percentage disputed by RDS.

-

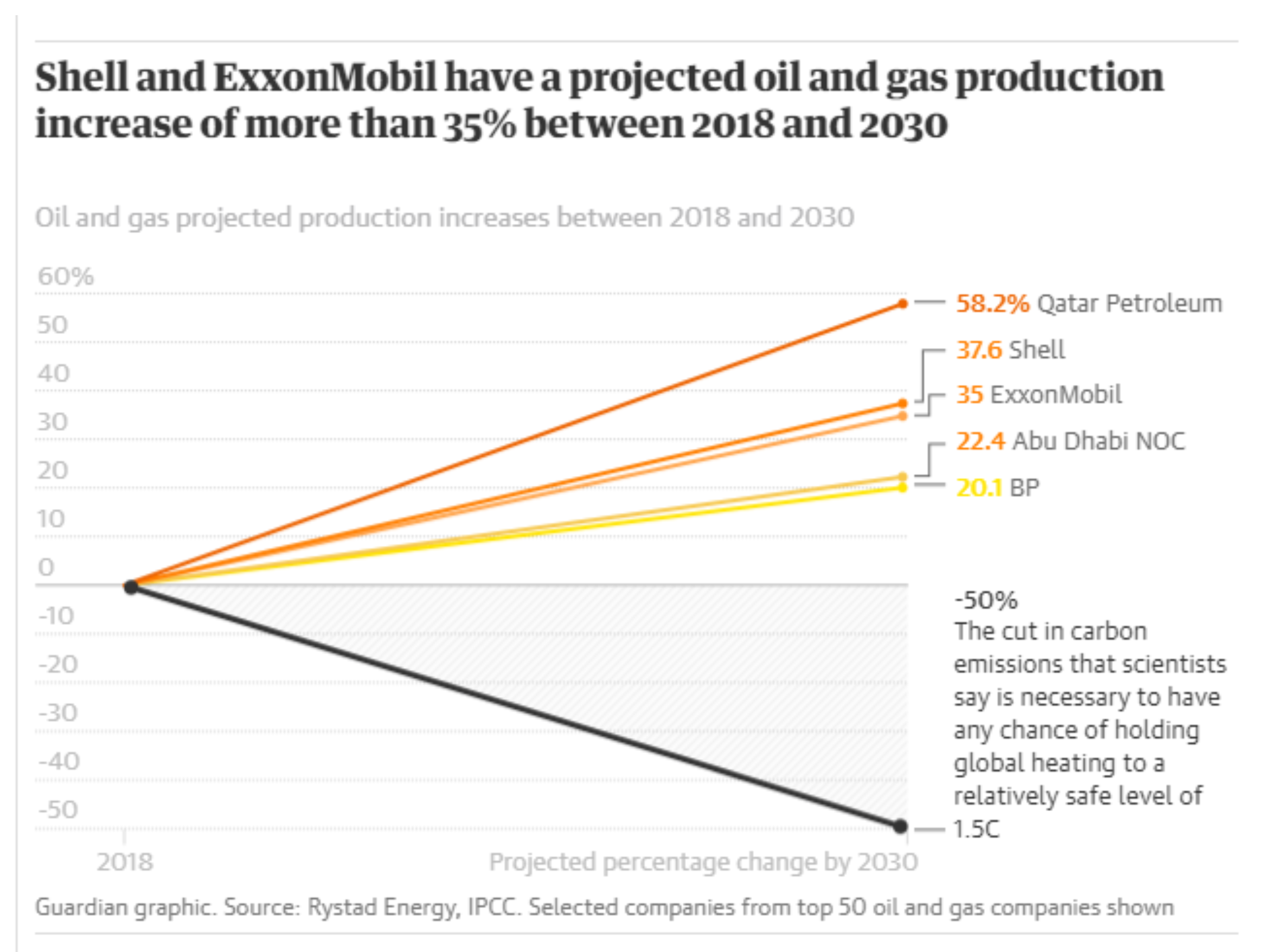

This percentage that RDS intends to maintain up to 2030 for its growing oil and gas activities, was also discussed in an article in The Guardian newspaper, which article Milieudefensie et al. has submitted into the proceedings as Exhibit 275. On the basis of research of Rystad Energy (of which The Guardian rightly says that it is a very reputable Norwegian consultancy firm), which produces data on the energy market and of which data RDS itself also makes use42, it appears that Shell and ExxonMobil jointly want to have their oil and gas production grow up to 2030 by more than 35% and that they are consequently the leading investors of the group of 50 biggest oil companies in the world. The other companies also want their oil and gas production to grow up to 2030, with which these 50 companies are making a move which is completely contrary to what is necessary to prevent dangerous climate change, according to the article in The Guardian. The article sets out the following figure of Rystad which makes it clear how the production growth of various companies, including RDS, stands in relation to the 1.5˚C goal.

-

In the ascending orange lines, this figure shows a growth percentage of 37.6% (rounded to 38%) for Shell and a growth percentage of 35% for Exxon Mobil. The black descending line shows what is necessary to limit warming to a maximum of 1.5˚C. This figure shows in one glance that Milieudefensie et al.'s previous statement, i.e. that RDS is on a collision course with the climate goal of Paris, is not an exaggeration.

-

Even though it is necessary for production to decline significantly to prevent dangerous climate change, Shell and other big oil and gas companies are fully gearing their investments in the coming decade to an enormous growth in oil and gas production, whereby RDS' production growth is thus expected to indeed grow by almost 38%. Whereas RDS' scope 1, 2 and 3 emissions should be drastically reduced, the emissions of the business activities and the products of the Shell group will in fact increase significantly as a result of this growth.

-

With the odd exception, all oil and gas companies want, just like RDS, to continue expanding their fossil activities. For that reason there is globally an enormous production gap between what may still be produced in fossil fuels under the Paris Agreement and what will actually be produced if oil and gas companies continue to invest as they intend to do. The evidence for this production gap is overwhelming and in this respect Milieudefensie et al. has submitted 6 reports as exhibits, all of which show the same picture, i.e. that the intended scope of investments in new oil and gas fields are completely at odds with the goal to still be able to prevent dangerous climate change (Exhibits 276, 277, 278, 280, 282, 333).

-

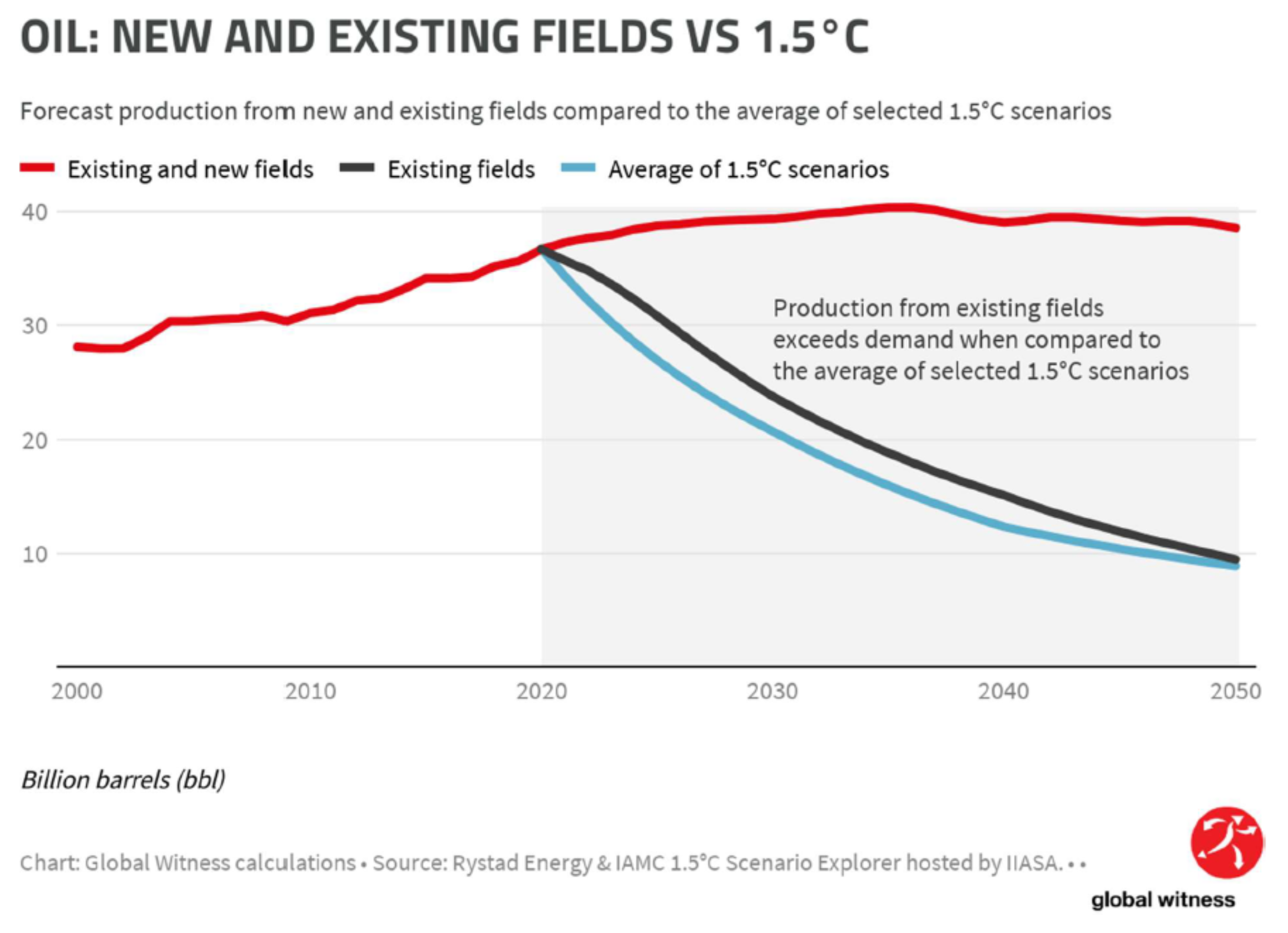

The Overexposed report of Global Witness, which has been submitted into the proceedings as Exhibit 277, clearly shows on the basis of data of the IPCC and Rystad Energy that the existing oil fields up to 2050 (in the event of an average forecast demand for oil over that period) will produce more than fits in with the goal of limiting the warming up of the earth to 1.5˚C .43 I will explain this on the basis of the following figure.

-

The blue line shows what oil production on average is still possible as a maximum in a 1.5˚C scenario.

-

The black line shows how the oil production of the current oil fields will run down to 2050 because the current oil fields will, of course, slowly run out. This black line shows that the existing oil fields alone will produce more in the coming 30 years than fits in with the 1.5˚C scenario.

-

The red line shows how much extra oil will be produced if the production of the new oil fields in which RDS and the other oil companies want to invest, is added to the existing oil fields. Up to 2030 the production will increase strongly and after that the production will remain high for decades. This has to do with the fact that oil fields are exploited for many decades.

-

The Production Gap report of UNEP and others, which has been submitted into the proceedings as Exhibit 276, sets out in the same sense the enormous production gap between a 1.5˚C scenario and the intended investments in new oil fields.44 The Production Gap report also shows that the intended investments are not only at odds with a 1.5˚C scenario, but they are also at odds with a 2˚C scenario.

-

According to the Production Gap report, the oil production will be a good 43% higher with the intended investments in 2040 than fits in with a 2˚C warming up of the earth.45 The intended investments in oil will thus bring the world past the 2˚C warming up. Although the 2˚C scenario can no longer be the guideline because of the far stricter temperature goal of the Paris Agreement, Milieudefensie et al. seeks to demonstrate with this that the intended investments in new oil fields that RDS and other oil companies have in mind, are in fact far removed from the oil production that would still be possible in a 2˚C scenario.

-

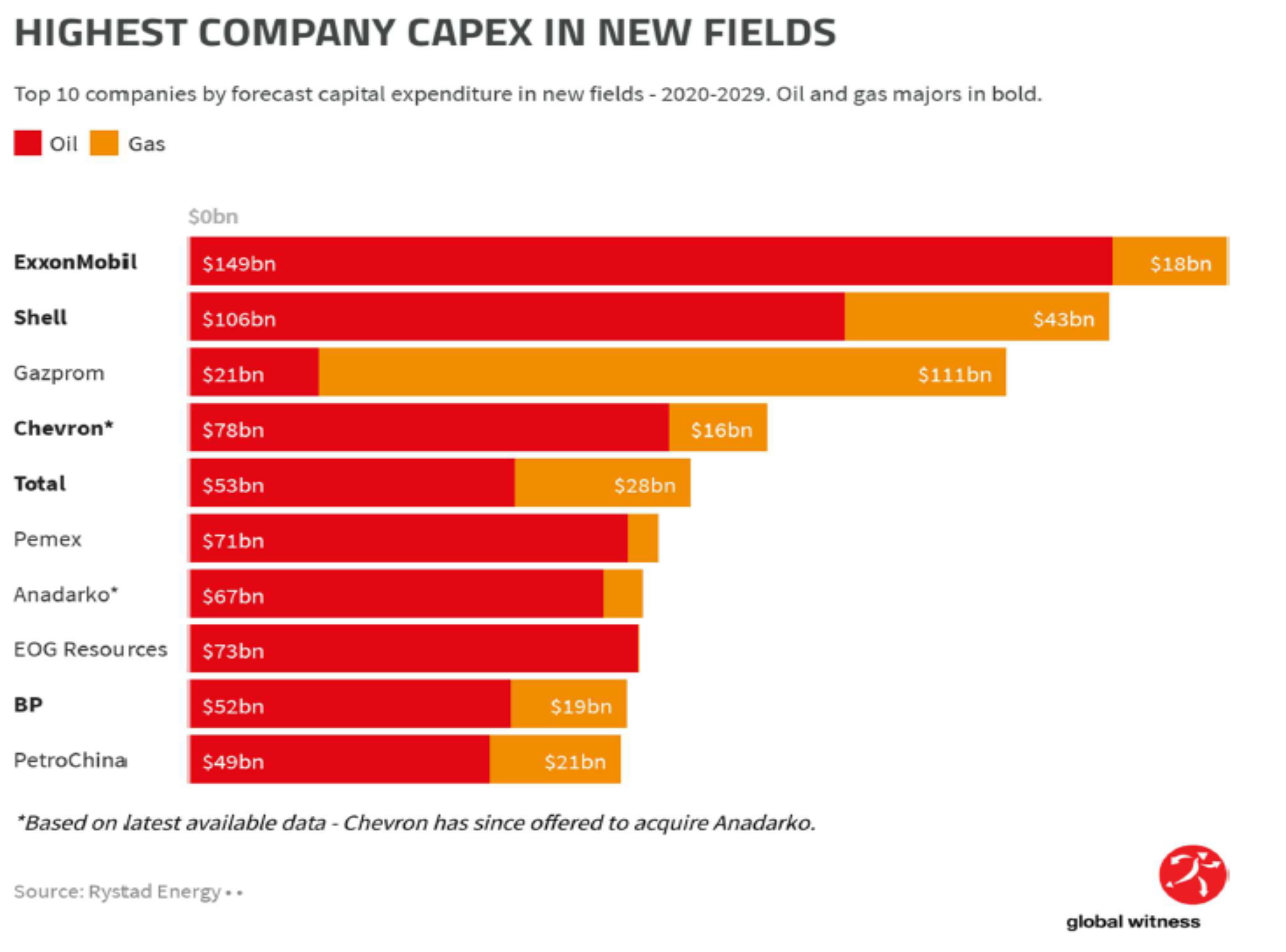

It is precisely RDS who for the coming 10 years is one of the two biggest investors in new oil fields. This also appears from the Rystad data, as the figure below illustrates.

-

This bar diagram sets out in red the intended investments up to 2030 in new oil fields. This diagram shows that RDS will have the Shell group invest US$ 106 billion in new oil fields. Only Exxon Mobil will be investing more than Shell. In comparison to BP, Shell will invest more than two times as much in new oil fields than, for example, BP or the Chinese State Oil Company PetroChina. BP recently stated to want to reduce the production in 2030 by 40%, so its investment position in oil will have decreased further in 2030.

-

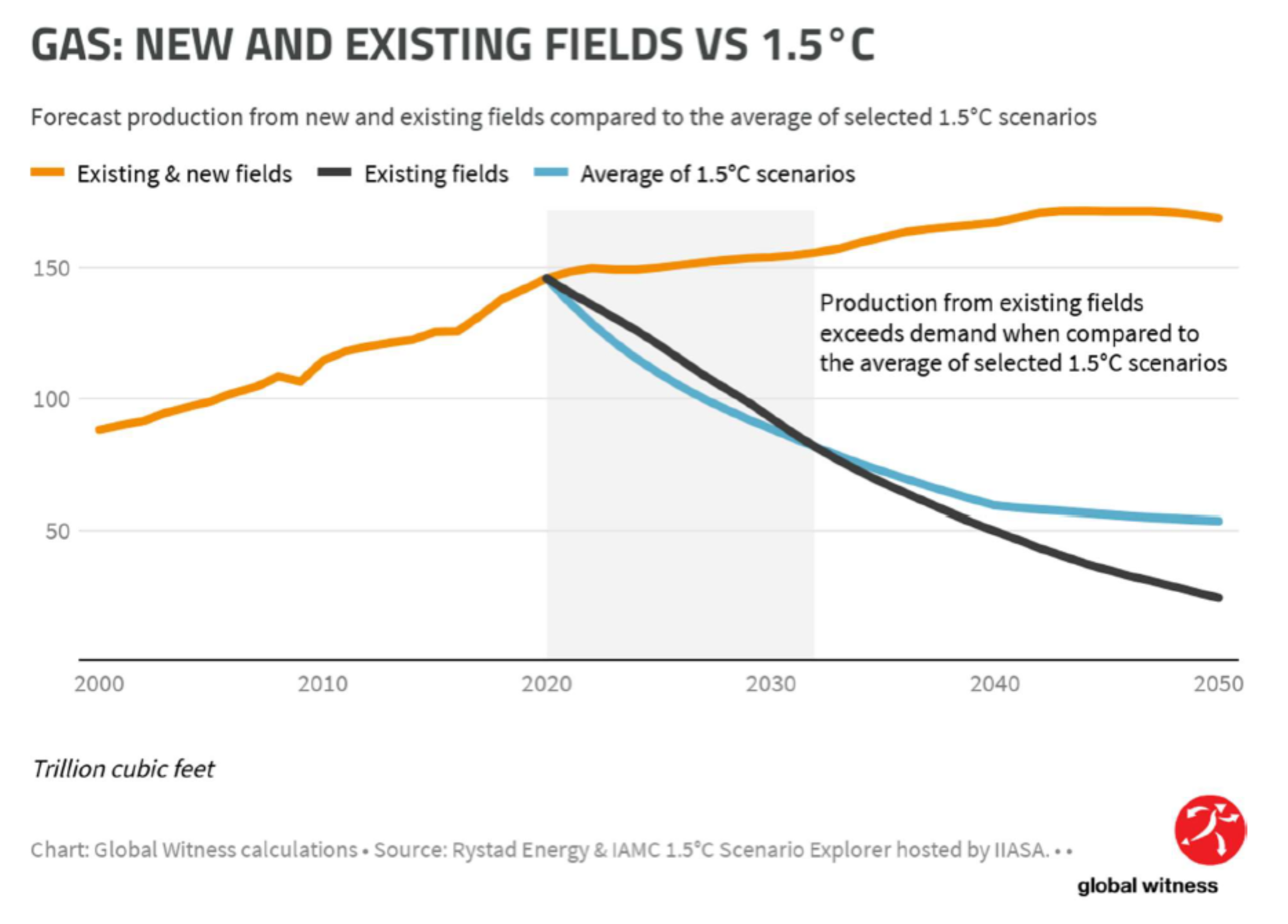

With regard to gas too, RDS' policy will lead to the Shell group being one of the two biggest investors in the world. Only the Russian Gazprom will invest more in gas. For the global gas production there is a comparable production gap as for oil, which is clarified in the figure below.

-

The blue line shows what maximum gas production on average will still be possible in a 1.5˚C scenario.

-

The black line shows how the gas production of the current gas fields will run down to 2050 because the current gas fields are slowly becoming empty. The black line shows that up to 2030 the existing gas fields will be producing more than fits in with a 1.5˚C scenario. After 2030, however, there will be some limited scope for new fields. This limited scope for investing in new gas fields is, however, only a fraction of what RDS and the other companies intend to invest in new gas fields. The latter is shown by means of the orange line.

-

With regard to the gas market it is the case that the intended investments in new gas fields are far removed from what is still possible in a 1.5˚C scenario. The UNEP Production Gap report and others once again show that this is also the case for the 2˚C scenario. According to the Production Gap report, 47% more gas will be produced in 2040 than fits in with a 2˚C scenario.46 The same picture follows from the other reports which have been submitted which discuss the production gap, as the picture presented by the Production Gap report and the Overexposed report of Global Witness.47

-

Because RDS is one of the biggest investors in both the oil market and in the gas market, it thus contributes to a significant degree to the creation of the ever-increasing production gap in the oil and gas market. With the production growth in oil and gas of 38% as of 2030 as foreseen by RDS, the scope 1, 2 and 3 emissions of the Shell group will in principle increase accordingly. In the coming decade, RDS will thus contribute both to increasing the production gap and to increasing the emissions gap.

-

While the emissions of the Shell group must decrease drastically to help prevent dangerous climate change, the emissions will in fact be moving in the opposite direction and continue to increase in scope. I will now explain this point in further detail, against the background of RDS' Net Carbon Footprint ambition, which does not mitigate this growth in emissions, let alone that this ambition of RDS will lead to a reduction of the CO2 emissions of the Shell group.

1.c Shell's Net Carbon Footprint ambition does not lead to a reduction in absolute emissions

-

Milieudefensie et al. explained in the summons why RDS' Net Carbon Footprint ambition is not sufficient. First, it is not a target, but an ambition. Ben van Beurden, the CEO of RDS, made this clear back in 2017 at the launch of the ambition.

This is an ambition for Shell, not a target48,

he said at the time and this has not changed, as was confirmed on behalf of RDS on day 2 of the court sessions. RDS cannot be obliged to comply with that ambition, so it is uncertain whether it will implement it.

-

The ambition is thus not an enforceable target. Indeed, it is not even an unconditional ambition. RDS does not want to commit itself even on this point. The ambition is a conditional ambition because RDS only wants to move at the speed at which society progresses in the transition. RDS particularly has an eye on the speed at which the consumer demand change or the speed at which national states proceed to implement regulations. RDS thus wants to follow, rather than participate in leading the energy transition. States and consumers are, in its opinion, the leading parties in the transition and it will adapt accordingly, that is what the conditional ambition of RDS entails in its core.49 To emphasise the "follower" character of its ambition, RDS keeps using the words "in line with society" or the words "in step with society" or the words "in step with society and its customers".50 For that reason too, the ambition provides no solid ground.

-

RDS' climate ambition is, moreover, not based on an absolute reduction in emissions but is only based on a relative reduction in emissions. The difference between the two has been explained in the summons and that difference is crucial and all-decisive.51 It has been explained in the summons that the ambition to achieve a relative reduction in emissions can be accompanied by an increase in absolute emissions. This even though the approach to the climate problem can only be successful if absolute emissions are reduced. There cannot be any discussion about this and that is a hard fact that no one can deny. RDS knows this too.

-

That for that reason RDS' ambition does not have any functional value in terms of preventing dangerous climate change, also appears from the fact that the collective scope 1, 2 and 3 emissions of the Shell group had increased by 5.4% at the end of 2019 compared to the base year chosen by RDS of 2016.

-

Over a period of four years the scope 1, 2 and 3 emissions of the Shell group increased from 733 million tons of CO2e in 2016 to 773 million tons of CO2e in 2019.52 This is an absolute increase in emissions of 5.4% over a period of three years, i.e. an average annual increase in absolute emissions of 1.8% per year.

-

In that same period of three years between 2016-2019, the net carbon footprint of the Shell group fell by 1.2% or by 0.4% per year.53

-

Thus even though the carbon footprint has fallen by 0.4% per year, absolute emissions increased by 1.8% per year. This shows why it is necessary to compel RDS to bring about reductions in absolute emissions, because these will otherwise not be effected. If the production of oil and gas increases by 38% in 2030, the emissions in 2030 will have increased considerably, even if in 2030 RDS would be on the way to having the emissions intensity of its scope 3 emissions fall by 30% in 2035, as it announced in its most recent ambition (Exhibit RK-32A, which also shows that such an ambition for 2035 was not formulated for scope 1 and 2 emissions).

-

Against this background it should also be clearer for the District Court why year after year the RDS board of directors emphatically advises voting against the shareholders' resolutions of Follow This and calls upon all of its shareholders to vote against the resolution which would oblige RDS to have the absolute CO2 emissions of the Shell group decrease in line with the Paris goal.54 And year after year, the great majority of the shareholders heed the advice of the RDS board.55 There can be no clearer proof that RDS has no intention whatsoever to reduce the absolute CO2 emissions of the Shell group and its products. Anyone who wants further proof can also review RDS' CDP report for 2020, in which RDS presents a statement for the years up to and including 2022 and indicates that in an absolute sense no emissions reductions will take place over this period.56

-

There can be no clearer proof that RDS has no intention whatsoever of reducing the absolute CO2 emissions of the Shell group and its products. Anyone who wants further proof can also review RDS' CDP report for 2020, in which RDS presents a statement for the years up to and including 2022 and indicates that in an absolute sense no emissions reductions will take place over this period.57

-

RDS knows that we are heading into the last decade in which dangerous climate change can still be prevented and knows what destruction humankind and the environment will undergo if this danger is not avoided. But in its most recent CDP report of 2020 it again informed the world that no emissions reductions need be expected of it in the coming years. This means that 1/5th of the most crucial decade in the climate approach will again be squandered.

-

It shows how important it is that the order to reduce emissions that Milieudefensie et al. is claiming, is granted. I will speak about the reduction claims and the related issues, after the break.

Counsel

Footnotes

-

See, inter alia, Chapter VIII.2.1.5. of the summons ↩

-

Summons, inter alia para. 41 in conjunction with 609-618 ↩

-

See opening arguments, notes on oral arguments 1, inter alia paras. 31-82 and paras.111-115 ↩

-

See with regard to scope 1, 2 and 3 emissions the summons under para. 810 and the statement of defence under para. 96 ↩

-

See opening arguments, para. 34 ↩

-

Summons, paras. 565-571 ↩

-

Exhibit 282, p. 5, table 1, 5th column from the left. ↩

-

Statement of 6 November 2020, para. 36 with a reference to Exhibit 270, p. 32 ↩

-

Exhibit 270, p. 32 ↩

-

Ibid ↩

-

Ibid ↩

-

Opening arguments, notes on oral arguments 1, para. 130 et seq. ↩

-

Exhibit 286, p. 1 ↩

-

Exhibit 286, p. 2 and the list of parties set out there, the "leading networks and initiatives from across the climate action community--driven by science" ↩

-

Exhibit 287, Oxford analysis, Table 1, under Scope and further clarification under 1.1. ↩

-

Exhibit 287, Oxford analysis, Table 1, under Timing and further clarification under 1.2 and 1.7 ↩

-

Exhibit 287, Oxford analysis, under 2 under Timing ↩

-

Ibid under Equity and this quote for further clarification under 1.4 ↩

-

Exhibit 287, Race to Zero Paper, p. 2 ↩

-

Exhibit 270, paras. 71 and 71. ↩

-

Exhibit 287, Oxford analysis, under Governance and further clarification under 1.7. ↩

-

Opening arguments, notes on oral arguments 1, paras. 130. et seq. ↩

-

Opening arguments, notes on oral arguments 1, paras.130 et seq. ↩

-

Summons, inter alia paras. 609-618, notes on oral arguments 3 (IPL section), paras. 50-53 with reference to Exhibit 314 in which p. 4 sets out the following regarding non-state decision making: "Their decision-making structures can also make them both more ambitious and nimbler than many nation states." ↩

-

Ibid ↩

-

Exhibit 273, p. 327 at the bottom and 328 at the top. ↩

-

Exhibit 322 ↩

-

Exhibit 286, pp. 1 and 2 ↩

-

Exhibit 322, p. 2 ↩

-

Exhibit 322, p. 2 ↩

-

Exhibit 322, p. 5 ↩

-

Exhibit 322, p. 6 ↩

-

Exhibit 322, p. 6 ↩

-

Statement of defence, para. 25 ↩

-

Exhibit 322, p.14 under category 11 (Use of sold products). ↩

-

In its report on the scope 3 emissions, Shell applies the usual standard category classification which is connected with scope 3 emissions. RDS' report on its website uses the same category classification as that which is set out on p. 14 of Exhibit 322 and which is represented in this manner as standard in the world, for example also in the Greenhouse Gas Protocol that RDS uses for its scope 1, 2 and 3 report. See also RDS' statement of defence under para. 98. ↩

-

Exhibit 322, p. 22 "At this stage it is important to consider how to engage with suppliers: 1) enforcing, 2) being supportive/informative, or 3) inducing competition among suppliers. The first approach is appropriate for larger high revenue companies that have leverage over their direct suppliers, while the second and third approaches are suitable for all companies." (underlining added by counsel) ↩

-

See opening arguments, notes on oral arguments 1, paras. 46-48 ↩

-

Exhibit 279, p. 2 at the bottom and p. 3 at the top ↩

-

Exhibit 316, pp. 6 and 7 ↩

-

See, inter alia, Exhibit RK-7 p. 35 ↩

-

Exhibit 277, p. 2 ↩

-

Exhibit 276, p. 4 ↩

-

Exhibit 276, p. 4 ↩

-

Exhibit 276, p. 4 ↩

-

See for the other reports, e.g., Exhibit 278, p. 11 and Exhibit 280, pp. 37 and 40. ↩

-

See further the summons, para. 808 ↩

-

See also statement of defence, paras. 106-109 ↩

-

See Exhibit 316, p. 7, Exhibit RK-32A and Exhibit RO-281, press release, p. 1 ↩

-

Summons, Chapter XI.4 ↩

-

For scope 1 and 2 emissions over 2016-2019, see the RDS report

For scope 3 emissions in 2016, see the RDS CDP report of 2017 from pages 60-65

For scope 3 emissions in 2019, see the RDS CDP report of 2020, from pages 110-118 ↩ -

See the first link in the note above. In 2016 the Net Carbon Footprint (gCO2e/MJ) was 79 grammes and in 2019 it was 78 grammes. ↩

-

Exhibit 316, pp. 6 and 7 and summons, 809-814 ↩

-

Exhibit 317 and summons, 809-814 ↩

-

RDS' CDP report for 2020, pp. 57 and 59 for the years 2021 and 2022 ↩

-

RDS' CDP report for 2020, pp. 57 and 59 for the years 2021 and 2022 ↩